Investing in AffordabilityCombating the national housing shortage using federal credit

A federal housing affordability investment facility could rewrite private incentives to shift the cost curve for affordable housing by deploying patient, low-cost capital fully backed by the federal government. This white paper outlines how catalytic federal financing could enable the full spectrum of housing providers to preserve at-risk affordable housing and create new homes in communities nationwide.

Introduction

A. The Case for Market Innovation

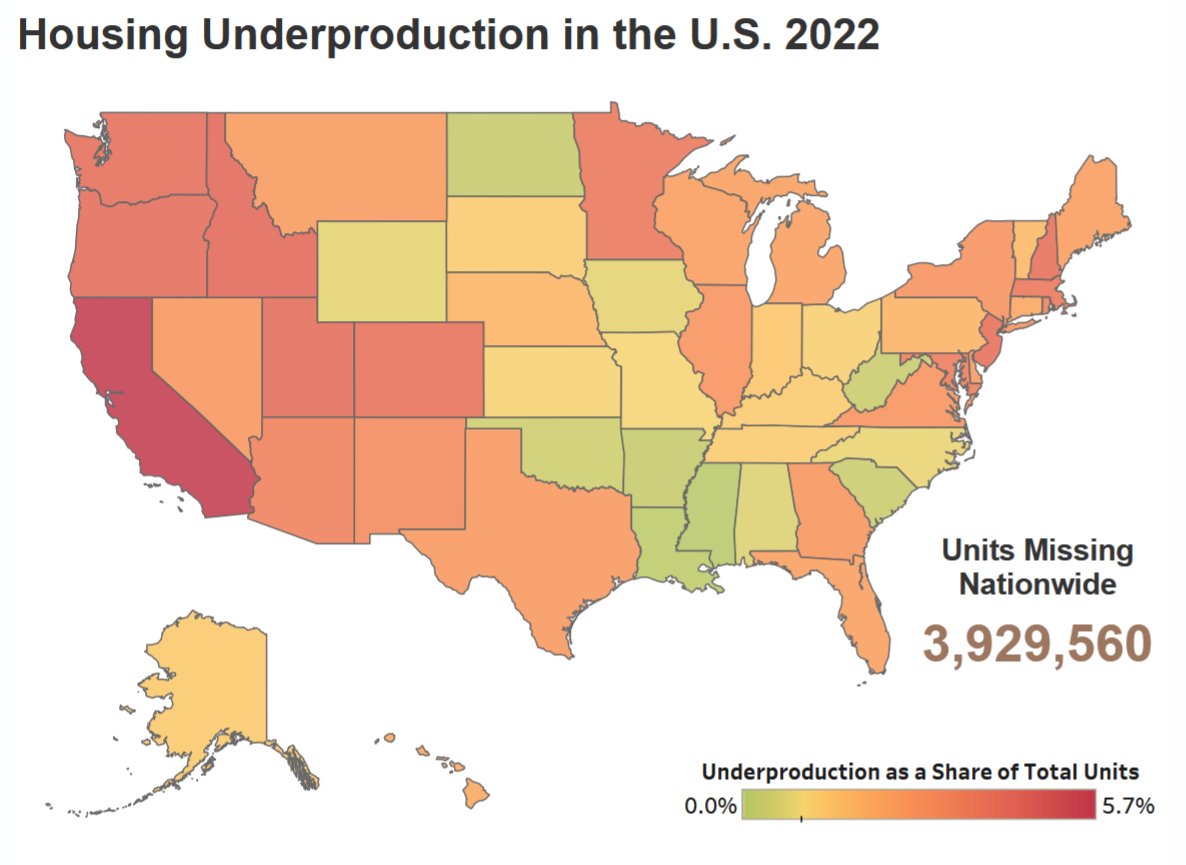

The United States faces an estimated supply gap of nearly 4 million homes1 and a shortage of 7.3 million housing units affordable for lower-income renters.2 Despite recent federal spending ranging from $50 and $90 billion on affordable housing programs, only one in every four households that qualifies for federal housing assistance receives support.3

The market forces driving development exacerbate our national supply shortage. Private investors maximizing profit are incentivized to select housing projects that create the highest financial returns with the lowest risk, while broader rent increases have grown unsustainable for low- and moderate-income (LMI) families.5

A federal housing affordability investment facility could rewrite private incentives to shift the cost curve for affordable housing by deploying patient, low-cost capital fully backed by the federal government. This catalytic financing would enable and incentivize the full spectrum of housing providers — from institutional investors to community-based nonprofits — to rehabilitate aging properties, preserve at-risk affordable housing, and create new homes in communities nationwide.

Though state and local coalitions have advanced legislative solutions to reduce barriers to development,6 we still lack federal financing and policy tools to unlock private investment that preserves and creates affordable housing at the scale and speed our country needs. This framework envisions a national investment program focused on expanding affordable and mixed-income housing supply by providing low-cost capital at the fund level, guaranteed by the federal government.

When we align financial incentives with housing affordability, we can unlock the power of private capital to deliver public good.

When we align financial incentives with housing affordability, we can unlock the power of private capital to deliver public good. Investors achieve competitive returns, mission-driven organizations scale their impact, and millions of families gain access to quality, affordable homes near jobs and opportunity.

B. The Affordable Housing Shortage

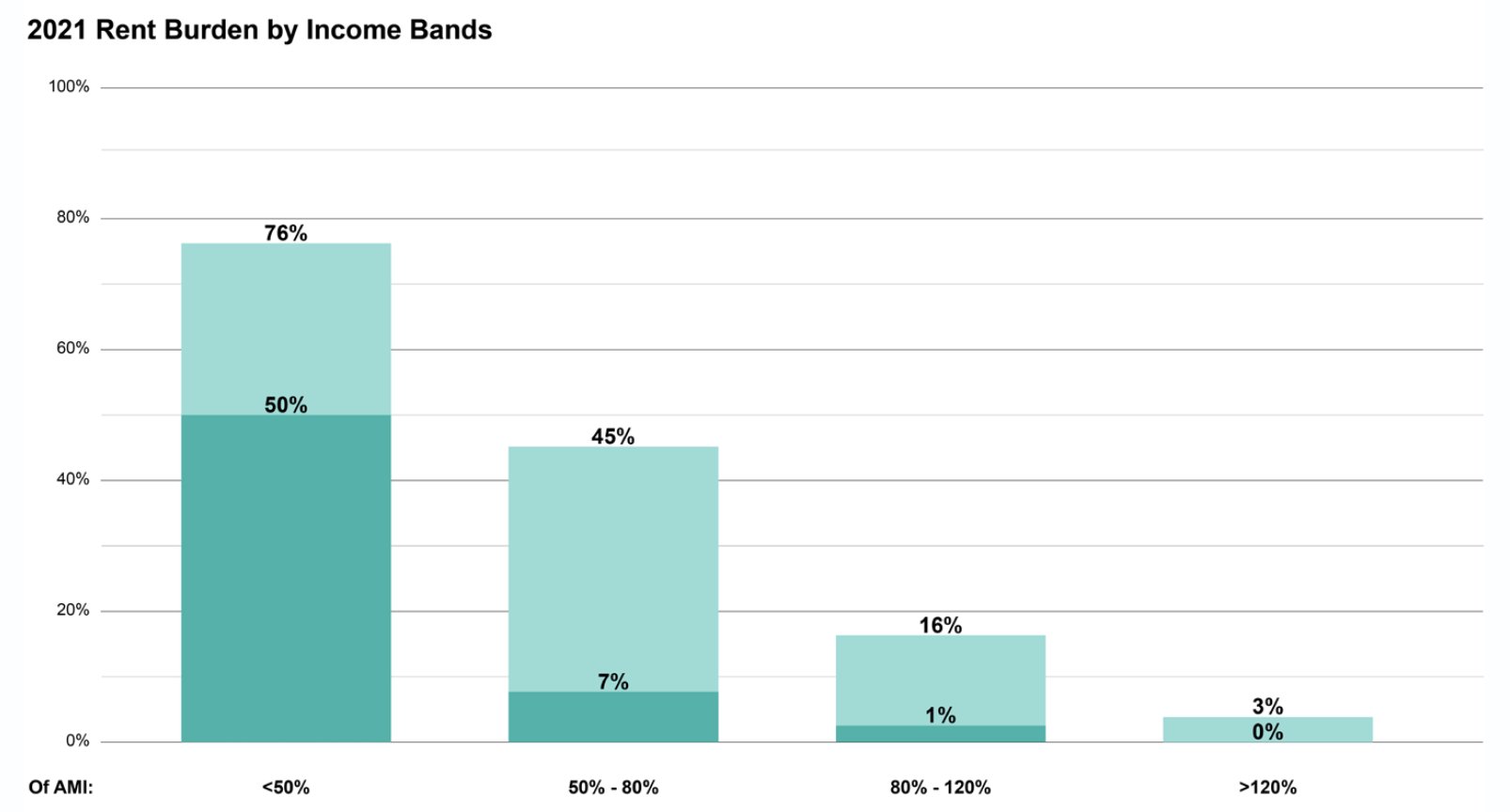

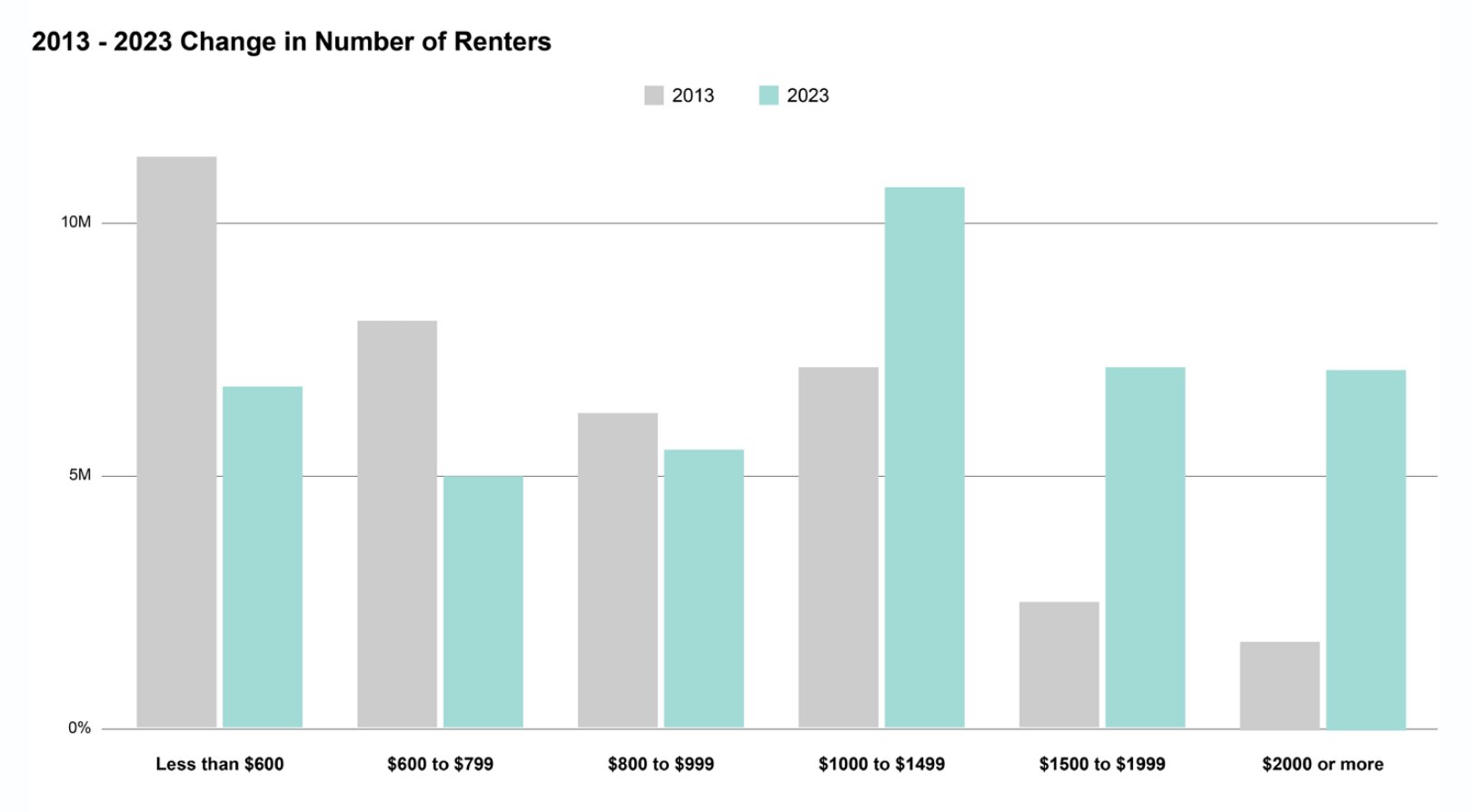

The scale of America's housing shortage has reached crisis levels, impacting households across the income spectrum. The majority of U.S. states do not have enough housing supply to meet demand, with most states remaining below pre-pandemic supply levels.7 A rising number of households, both renters and homeowners, pay more than 30 percent of their paycheck on housing — formally qualifying as "cost burdened." Nearly 50 percent of all renter households in the United States, regardless of income, are cost-burdened.8 Another 12.1 million renters are extremely cost-burdened, spending more than half their paychecks on housing costs alone.9 These burdens are especially widespread for low-income households — 76 percent of low-income renters are cost-burdened10 — But the nation's housing crisis also impacts households further up the income spectrum. In recent years, rent burdens have risen most dramatically for moderate-income families, doubling for households making between $45,000 to $74,999 between 2001 and today.11

Cost burdens reveal the kitchen-table impact of these shortages. After making their rent payments, 65 percent of working-age renters do not have enough left for everyday essentials;12 the average low-income renter in the U.S. only has $310 per month remaining for any other expense.13 The cost pressures imposed by the affordable housing shortage represent a threat to the resilience of the U.S. economy, limiting workforce mobility and undermining economic growth.

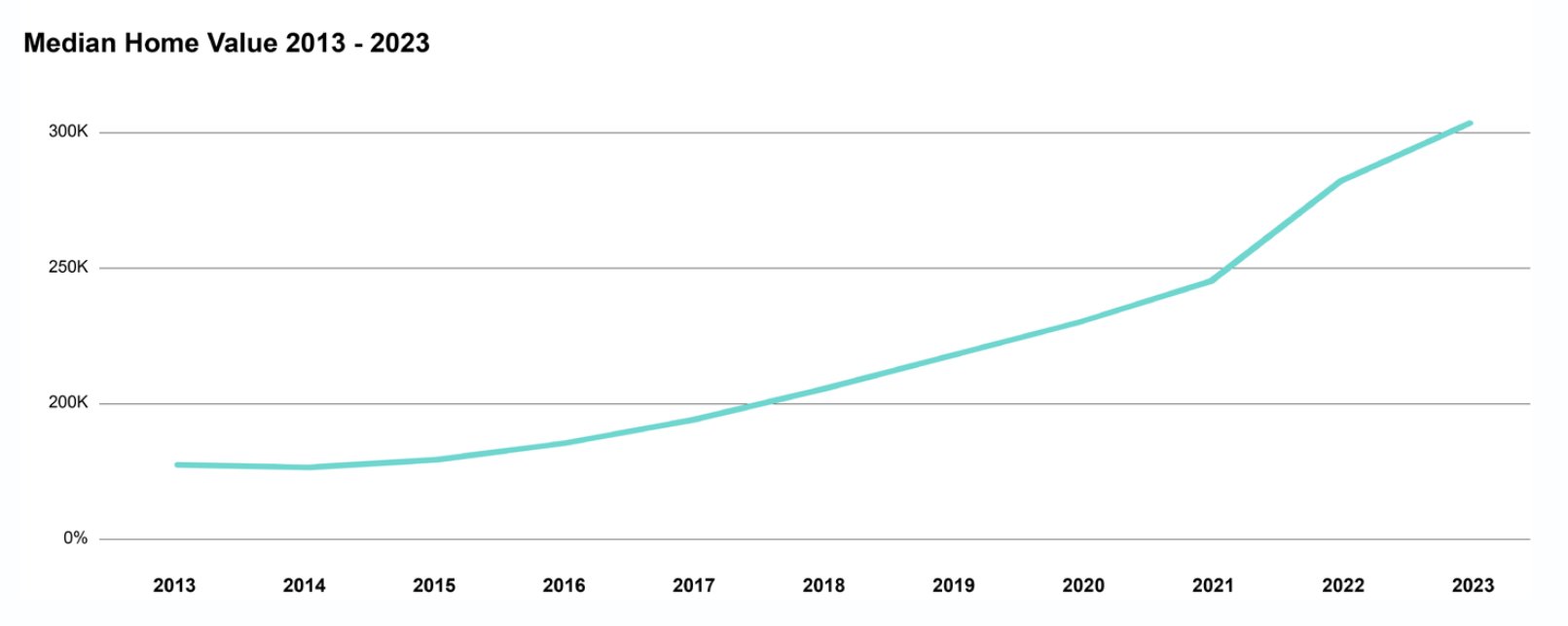

While high rent prices erode household savings, limited construction of new, affordable for-sale homes places in jeopardy economic advancement and wealth creation through homeownership. Lack of both affordability and access to homeownership also contribute to delayed household formation, with young Americans postponing milestones like parenthood, unable to afford homes suitable for growing families.14 Life-cycle models have suggested that when households' perceived probability of becoming a homeowner falls out of reach — called the "giving up" threshold — systematic behavioral shifts occur that undermine long-term financial stability.15 If unchecked, these structural issues threaten the viability of the American Dream across generations.

Geographic disparities underscore the multifaceted and complex nature of America's housing supply shortage. Rural home prices increased faster than the national average between 2020 and 2023, with low construction rates, aging, inadequate stock, and limited mortgage financing undercutting supply.17 The consequence: the rural housing shortage exceeded 456,000 units in 2022.18

Meanwhile, high-cost urban areas have grown more unattainable. The pandemic fueled an acceleration of post-Great Financial Crisis price trends, with tightening inventories and sustained price inflation rapidly compounding housing prices.19 Coupled with rising costs of living and stagnating wages, LMI households have become increasingly locked out of rental and homeownership markets, limiting their economic mobility and financial security.20

C. How Affordable Housing is Financed

Guaranteed loans have been central to the American housing system for nearly a century. Established in 1934, the Federal Housing Administration (FHA) was created to increase access to mortgages to enable homeownership.21 FHA loans are designed for low-income and first-time home buyers and Department of Veterans Affairs (VA) loans are designed for veterans of the US military.22 As of June 2025, of the $12.94 trillion in outstanding mortgage balances in the United States, loans securitized by government sponsored entities like Fannie Mae and Freddie Mac make up over half of all balances, roughly $6.2 trillion.23 Government-backed loans, like those insured by the FHA or the VA, make up 19 percent of mortgages, $2.5 trillion in outstanding balances.24

For affordable rental housing, federal financing operates through a complex ecosystem dominated by the Low-Income Housing Tax Credit, or LIHTC. LIHTC represents the nation's largest and most prevalent federal rental housing subsidy, with an annual cost of $15.2 billion generating roughly 115,000 affordable units annually.25 LIHTC has successfully leveraged more than $100 billion in private equity investment since 1986 — a victory for affordability nationwide — yet broader production in the housing market declined to roughly two-thirds of historic levels, even with elevated demand.26

LIHTC can be used to build new housing or rehabilitate existing buildings and is structured to subsidize either 30 or 70 percent of the cost of the housing units in a qualifying project, depending on the type of credit used.27 But developers often must secure additional layers of financing beyond LIHTC to make their projects financially feasible, or "pencil." Among the roughly 1 million LIHTC units constructed from 2000 to 2021, only 55 percent used LIHTC as an exclusive funding source.28 Making a project pencil often requires assembling a complex capital stack that can include up to 20 sources of funding, creating significant barriers in access to capital for financing affordable housing projects.29

Today, more than 250 unique affordable housing programs – including state and federal subsidies — are layered to make projects affordable for LMI families.30 This complicated stack of funding sources creates significant inefficiencies. Developers not only have to win LIHTC financing from housing finance agencies, they must also demonstrate they can qualify for these other limited sources of support when applying for credits. That process can delay project starts by months and even years, driving up the costs of development and slowing the creation, preservation, or rehabilitation of affordable units.31 Conversely, market-rate developers can access simpler, more streamlined capital structures at a faster pace — impeding the ability of mission-driven organizations to compete for land or construction partners. Although Congress expanded LIHTC during the 2025 federal budget reconciliation process and may now be able to finance an additional million affordable rental homes,32 that increased production still only represents a fraction of today's need.

D. Shortcomings in Today's Housing Market

Current market forces systematically favor housing types that preclude LMI renters and homeowners, creating severe supply-demand gaps that exacerbate the housing shortage. In the last quarter of 2024, roughly half a million luxury apartments were under construction nationwide, compared to only 6,700 more affordable units with average monthly rents of $1,332 — a 70:1 ratio favoring high-end development.33 Although luxury units face double the vacancy rate of their more affordable counterparts,34 developers are still finding the higher margins in mid and premium segments more attractive. This supply shift has resulted in a decrease in the total number of units affordable to the lowest-income groups in the United States, despite apartment construction reaching a 50-year high in 2023 of 996,000 units under construction.35 The new construction of total development has been shown to have a "filtering" effect – decreasing rents at lower-ends of the spectrum.36 But the immediate need for housing that is affordable for LMI households is not being met by market forces and current programs and policies.

Federal Investment as a Market-Shaping Tool

A. Federal Credit Programs

Federal credit programs provide $1.9 trillion in assistance through 129 programs across various sectors, demonstrating the government's extensive track record in managing credit risk.37 Because the federal government holds a unique position in the market — a high credit rating, the capacity for patient lending, and the ability to smooth losses across economic cycles — it is uniquely positioned to attract private capital for public good at unmatched scale.

Federal credit programs differ fundamentally from direct spending programs in their ability to leverage private capital while maintaining market discipline. Rather than replacing private investment, credit programs can crowd-in private capital by reducing risks and costs preventing market participation. This approach preserves investor due diligence and portfolio management, while addressing market failures that prevent socially beneficial investments. And, because of their statutory requirements, well-designed credit programs can achieve these transformative policy goals at minimal or even positive returns to taxpayers: operating at zero subsidy cost.

B. The SBIC as a Policy Model

The Small Business Investment Company (SBIC) program provides a compelling precedent for how a federal investment facility could mobilize billions in private capital towards affordable housing preservation and development, while generating positive returns for taxpayers.

Since its inception in 1958, the SBIC program has facilitated over $130 billion in investments across nearly 200,000 small businesses.38 The program has generated a net surplus of over $1.2 billion for the federal government over the past 24 years, demonstrating the power of credit programs to achieve policy objectives while protecting taxpayer interests.39

The SBIC's program mechanics offer a direct template for affordable housing applications. Licensed participants in the program ("SBICs") raise private capital and then leverage this capital with SBA-guaranteed debentures at a 2-to-1 ratio.40 The SBA provides 100 percent guarantees on the debenture principal and interest, enabling SBICs to access low-cost debt at Treasury rates plus a modest spread.41 This leveraged capital structure allows fund managers to generate competitive returns even when investing in higher-risk or lower-return opportunities that align with policy objectives. Performance data validates the SBIC model's effectiveness. SBICs outperform comparable non-SBIC peers by an average 4 percent internal rate of return, while achieving superior multiples on invested capital.42 This outperformance is particularly meaningful given SBICs' focus on underserved markets and smaller transactions that traditional private funds typically avoid. The program's success stems from its alignment of incentives: fund managers maintain full fiduciary responsibility to their investors, while the government's patient, low-cost capital enables longer investment horizons. The SBIC provides a roadmap for a flexible credit facility that would evolve with housing market needs.

C. The Benefits of Credit Facilities

Federal credit facilities offer complementary advantages to both direct spending programs and pure private market solutions, providing powerful tools for achieving housing affordability objectives at scale. By offering meaningful leverage — for example, two dollars in federally-backed, low-cost capital for every dollar in private funding raised — a credit facility both creates a multiplier effect on total capital available for investment while also lowering the cost of that capital at the fund level. Applied to housing, similar leverage ratios could mobilize billions in private capital to invest in approved affordable housing models.

This structure also allows the government to bear the market risks it is uniquely positioned to manage — like long-term economic cycles, systemic market disruptions, or policy uncertainty — while preserving private sector discipline in project selection, underwriting, and asset management. These cost and operational efficiencies drive stronger incentive alignment among developers and investors requiring sufficient returns, and public actors committed to expanding the breadth and depth of affordable housing supply. They also drive sustainable market changes by serving as "proof" to the rest of the market: once private investors observe successful performance in credit-enhanced portfolios, they may increase direct investment without enhancement. The SBIC's role in supporting venture capital exemplifies this demonstration effect, with private markets now investing in similar structures without federal support.43

This commercialization "proof" value could be especially meaningful for innovations in housing production and ownership, including construction modernization, resident-owned communities, and other pathways to wealth-building through profit sharing and renter wealth-building – models that may have found success in specific markets but have not yet found success attracting institutional capital at scale.

Credit Where It's Due: Applications to Housing

A. How a housing affordability investment program could work

A federal housing affordability investment program modeled after the SBIC could operate as a specialized facility providing patient, low-cost capital to qualified fund managers committed to affordable housing preservation and development. Drawing from the SBIC's proven framework, the facility would provide licenses through a rigorous vetting process evaluating track record, management capacity, and commitment to affordability objectives. These licensed entities would then raise private capital from private investors (pension funds, insurance companies, banks, impact investors, etc.). Then, the licensed entity could access federal leverage at the fund level.

The mechanics would mirror successful SBIC operations while addressing housing-specific needs. Licensed entities would raise initial private capital commitments — for example, up to $250 million per fund — and then apply for federal leverage. To illustrate, a 2:1 leverage ratio would allow a $250 million fund to access an additional $500 million in low-cost capital, or $750 million in blended capital at the fund level. This fund-level debt would be priced at Treasury rates plus less than 100 basis points, dramatically reducing the fund's overall cost of capital. The blended capital structure would enable licensed entities to invest in affordable housing projects via both debt and equity positions: generating sufficient returns to attract private investors, while maintaining or creating affordability for residents.

The U.S. Department of the Treasury's institutional advantages make it an optimal home for such a facility. The department's experience managing complex credit programs, sophisticated risk modeling capabilities, and established relationships with capital markets would accelerate implementation.

Eligible investments could encompass the full spectrum of affordable housing needs: new construction of single-family and multifamily homes in a wide range of market types, acquisition and preservation of existing affordable properties at risk of losing their affordability, rehabilitation of aging subsidized housing, and the expansion of promising, innovative models that have difficulty accessing capital at scale. Projects would be required to maintain affordability for extended periods, meeting specific income targeting requirements according to area median income. Treasury or the implementing agency could also explore geographic diversity incentives to ensure capital flows to both rural and urban markets, addressing the widespread nature of America's housing shortage.

B. Complementarity with Existing Programs

Accessing low-cost capital from the federal government at the fund level would streamline financing for affordable housing development, allowing licensees to blend low-cost capital from Treasury with private investment. A federal credit enhancement facility would also amplify the impact of existing affordable housing programs by deflating costs on projects already benefitting from or that would qualify for federal and state subsidies. The following examples illustrate how fund-level dollars could interact with popular affordable housing finance tools today:

The Low-Income Housing Tax Credit Program (LIHTC) generates approximately 115,000 affordable units annually at a cost of $15.2 billion. Unfortunately, hundreds of thousands of the 3.65 million units created over the history of the program are at risk of losing their affordability over the next 10 years. There is not enough tax credit capacity to recapitalize and extend the affordability of all these projects. Capital allocated via a federal investment program at Treasury could be used to recapitalize LIHTC projects with expiring affordability requirements. This would enable the preservation of affordability of thousands of units without having to use new, limited tax credit resources.

Opportunity Zones (OZs) are designed to spur economic activity by providing tax incentives to investors targeting designated communities.44 By achieving a license through the federal investment program, OZ funds would be eligible to use the benefits of both programs in tandem. Participants raising money from investors who benefit from the capital gains incentives of the OZ program would be eligible to receive 2:1 leverage from Treasury – for example, if the licensed entity raised $100 million from OZ investors, it would then be eligible for $200 million in low-cost capital from Treasury. These combined funds could then be invested in eligible affordable multifamily rental projects in Qualified Opportunity Zones, the distressed communities identified by the OZ program. These projects would be required to meet the federal credit facility's requirements for housing affordability.

Community Development Financial Institutions (CDFIs) are mission-driven financial institutions dedicated to providing capital to underserved and low-income communities. Certified by the Treasury Department, CDFIs aim to promote neighborhood revitalization and equitable development.45 They control $436 billion in total assets across 1,432 certified organizations.46 CDFIs come in several forms, including community development banks, credit unions, and loan funds. Credit enhancement could strengthen and amplify CDFI's missions to invest in deeply distressed markets. The Capital Magnet Fund's success in generating $30 for every $1 of federal funds demonstrates CDFI's leveraging capacity that a complementary investment program could advance even further.47

State Housing Finance Agencies are entities chartered by state government that help meet the affordable housing needs of their residents. Along with administering the LIHTC program and other public initiatives, many HFAs have created innovative public-private partnerships with private investors and operators to increase the supply of affordable housing. HFAs are crucial implementation partners with established infrastructure and local market knowledge, having delivered over $800 billion in financing historically and serving 250,000 – 275,000 households annually.48 A federal investment program could license investment funds created by HFAs, providing them with additional low-cost capital to advance their missions.

C. Incentive Alignment: Affordability and Accessibility

The design of a federal investment program must carefully align incentives to ensure that subsidized capital at the fund level translates into genuine affordability and expanded access for underserved people in overlooked places.

Applicants with the most compelling strategies to create the types of affordable housing needed in their target communities could be prioritized in the application and licensing process. Additional "bonus" leverage could be provided to reward fund managers who exceed affordability targets, provide resident services, or serve particularly challenging populations. Regardless, affordability maintenance will require robust reporting and enforcement mechanisms. Using the SBIC program as a guide, penalties for affordability violations could include accelerated debt repayment, loss of license, and potential clawback provisions.

Inspired by "Reinvestor" SBICs that are authorized to serve as fund-of-funds and provide equity to support smaller fund managers, emerging licensee programs could expand access beyond established players to next-generation developers and nonprofit organizations. Set-asides, mentorship and sponsorship structures could help develop a more diverse and resilient affordable housing ecosystem. Graduated requirements based on developer experience could balance risk management with opportunity expansion.

Finally, resident outcomes would prove central to performance reporting and monitoring—moving beyond unit counts to assess genuine impact upon housing stability and economic mobility. Metrics could include rent levels, household demographic information, eviction rates, average tenancy duration, and connections to supportive services. Licensees demonstrating superior resident outcomes could receive priority access to subsequent funds, creating competition based on impact rather than purely financial returns. This outcomes-based approach would ensure that federal investment in affordable housing achieves its ultimate purpose of improving lives, not just producing units.

Conclusion

The establishment of a federal housing affordability investment program represents a transformative opportunity to address America's housing crisis through proven financial mechanisms that mobilize private capital at unprecedented scale. The convergence of acute housing shortages affecting 7.3 million LMI households49 and the demonstrated success of the SBIC model generating positive returns for taxpayers50 creates optimal conditions for effective implementation.

A facility operating at Treasury using established authorities and proven risk management frameworks, would provide patient, low-cost capital to licensed fund managers committed to preserving and creating long-term affordability. By leveraging private investment 2:1, the facility could mobilize hundreds of billions in private capital, achieving far greater impact than direct appropriations alone. Integration with existing programs would multiply current federal investments while streamlining complex financing processes that impede housing production.

Critical design features would ensure mission alignment and fiscal responsibility. Performance-based incentives would reward deeper affordability and superior resident outcomes. Next-generation developer provisions would expand access to emerging and nonprofit firms. Robust compliance monitoring would maintain long-term affordability while preserving private sector efficiency in project selection and asset management.

This political moment demands bold action commensurate with the severity of the housing shortage. Federal credit programs and the SBIC model offer a scalable, market-based solution that can attract bipartisan support while delivering meaningful relief across every state. This framework presents an opportunity to shape market incentives towards one of the nation's greatest needs: spurring investment that generates positive returns for taxpayers while creating the affordable homes needed by millions of Americans.